The financial district of Singapore, where Nick Leeson traded for Barings on the SIMEX exchange. From a desk here, a single unsupervised young trader ran up losses that would destroy Britain's oldest merchant bank, founded in 1762 — hiding the damage in a secret account until an earthquake made it impossible to conceal. Wikimedia Commons / ProjectManhattan, CC0.

Nick Leeson and the Rogue Trader Who Broke a 233-Year-Old Bank

Singapore and London, 1992–1995 — Barings was Britain's oldest merchant bank, financier to the Crown for two centuries. A single 28-year-old trader in Singapore, hiding his losses in a secret account, gambled it all on the Japanese market — and an earthquake finished what his recklessness began

- Category

- Finance & Economy

- Published

- Length

- 3,700 words · 18 min read

- Author

- The editors

The Barings collapse is the archetypal "rogue trader" story, and it carries a lesson distinct from the accounting frauds and Ponzi schemes elsewhere in this archive. Nick Leeson did not, at least at first, set out to steal or to enrich himself through an elaborate con; he set out to hide a mistake, and then another, and then to gamble his way out of an ever-deepening hole — and in doing so he destroyed one of the oldest banks in the world. The deeper villain of the story is not just one reckless young man but the institution that gave him enormous power and almost no supervision, that cheered his fictitious profits without ever asking how they were made. Barings is the case study in what happens when the controls that are supposed to govern risk simply are not there.

This is the story of the trader who broke a 233-year-old bank.

Britain's oldest bank

To grasp the scale of what was lost, you have to understand what Barings was. Founded in 1762, it was a merchant bank of immense history and prestige — so important to Britain that it had helped finance the country's wars against Napoleon and had arranged the financing of the United States' Louisiana Purchase in 1803. It was banker to the British monarchy. A French statesman had once called Barings one of the six great powers of Europe. By the 1990s it was a smaller player than in its imperial heyday, but it remained a respected, aristocratic institution at the heart of the City of London, the kind of bank whose name was a byword for solidity and tradition.

It was the very solidity of Barings, the assumption that such an institution was inherently safe, that made what happened so shocking. A 233-year-old bank that had survived the Napoleonic Wars, two world wars, and countless financial panics was destroyed in a matter of days by the actions of one employee — an outcome that seemed almost impossible, and that exposed how a venerable name and a long history are no protection against a failure of basic controls.

The star trader in Singapore

Nick Leeson was, by the standards of Barings' patrician world, an outsider — a young man from a working-class background in Watford, without the elite education of the bank's traditional managers, who had worked his way up through back-office settlement roles. In the early 1990s he was sent to Singapore to run Barings' operations on the Singapore International Monetary Exchange (SIMEX), trading futures and options. And there he appeared to flourish spectacularly, reporting large and growing profits that made him a celebrated figure within the bank — the brilliant young trader whose desk in Singapore seemed to be a money machine.

The distance mattered. Leeson was thousands of miles from London, in a fast-moving derivatives market that his superiors back home poorly understood, operating with little effective supervision. To the bank's management, he was a remote source of welcome profits; few of them had the expertise to grasp what he was actually doing on the SIMEX floor, and the physical and managerial distance meant that the normal frictions and questions that might have surfaced a problem were absent. He was, in effect, left alone with enormous power and almost no one watching — a combination that, in finance, is a recipe for ruin regardless of the character of the individual involved.

This is where the first and most fundamental failure lies. Leeson was put in charge not only of trading — making the bets — but also of the back office that settled and recorded those trades. In any properly run financial institution, these functions are rigorously separated: the people who make trades must never be the same people who confirm, settle, and account for them, because combining the roles removes the basic check that stops a trader from hiding what they are really doing. Barings, in a catastrophic lapse, let Leeson control both. He could make trades and then, in effect, mark his own homework — recording, settling, and concealing them himself. The door to disaster was left wide open.

The 88888 account

The mechanism of concealment was a secret account. Early on, Leeson used an error account — a type of account meant to temporarily hold trading mistakes — numbered 88888 (a number considered lucky in Chinese culture). Into this account he began to hide losses, keeping them off the books that Barings' management and auditors saw. What may have started as the concealment of relatively small errors grew, as losses mounted, into the hiding of catastrophic sums.

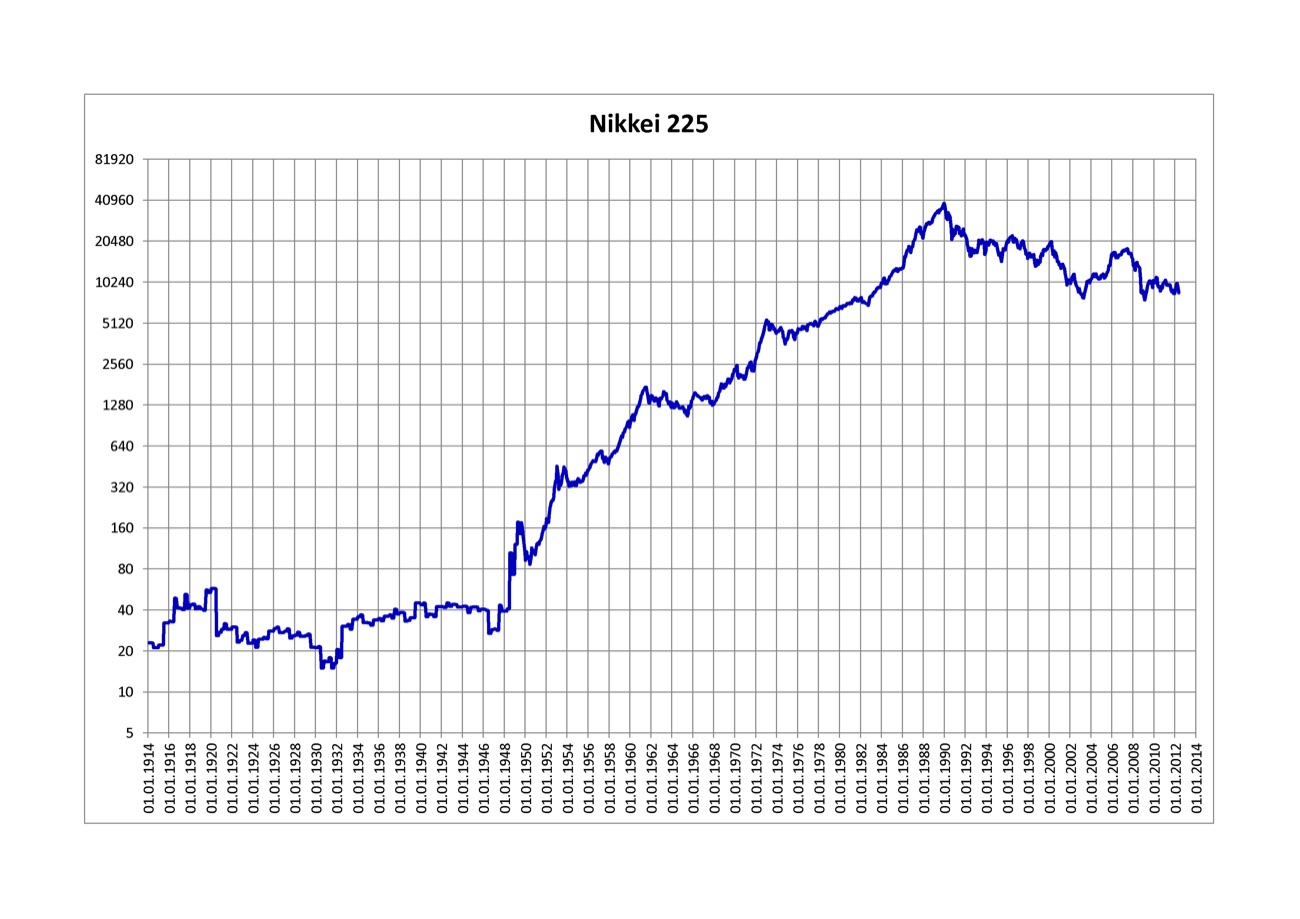

To dig himself out, Leeson did what desperate traders do: he gambled bigger. He took ever-larger positions, betting heavily that the Japanese stock market, the Nikkei index, would stay stable or rise — a wager that, if it came good, might let him recover the hidden losses and make everything whole. He sold options and built enormous futures positions on that assumption. And the truly damning part is that Barings' London management not only failed to detect the hidden losses but actively fed the disaster: believing Leeson's reported positions were profitable and properly hedged, the bank wired him enormous sums of money to meet the margin calls on his trades — funding, without realising it, an ever-deepening catastrophe. By early 1995, Leeson's bet on a stable Japanese market had become colossal. He needed the market to stay calm. Instead, the ground shook.

The Kobe earthquake

In the early morning of 17 January 1995, a massive earthquake — the Great Hanshin earthquake — struck near the Japanese city of Kobe, killing thousands and causing immense destruction. Beyond the human tragedy, the disaster sent a shock through Japan's financial markets: uncertainty and fear drove the Nikkei index sharply down, exactly the kind of volatile, falling market that Leeson's enormous positions were betting against.

For Leeson, the earthquake was financial catastrophe. His positions had been built on the assumption of a stable market, and now the market was anything but. As the Nikkei fell, his losses exploded. In a final, desperate gamble, he reportedly increased his bets even further, trying to single-handedly prop up the Japanese market or to bet on its recovery — and lost even more as it continued to fall. The hidden losses in account 88888 ballooned beyond anything that could be concealed or covered, ultimately reaching about £827 million — more than the entire capital of Barings Bank. The hole was now bigger than the bank itself.

The collapse

By late February 1995, the game was up. Leeson, realising the scale of the disaster and unable to hide it any longer, fled Singapore with his wife, leaving behind a note that simply said "I'm sorry." As Barings' management finally uncovered the true state of the 88888 account, they were confronted with the impossible: losses that exceeded everything the bank had. There was no way to absorb them. A 233-year-old institution, banker to kings, was insolvent because of one trader's hidden bets.

Frantic efforts to save the bank over a weekend — including appeals to the Bank of England to organise a rescue — failed, because the losses were simply too large. On 26 February 1995, Barings collapsed. It was declared insolvent and placed into administration, and shortly afterward the entire bank was sold to the Dutch financial group ING for the nominal sum of one pound. The name Barings, which had stood at the summit of British finance since before the American Revolution, effectively vanished. Leeson, meanwhile, was arrested in Germany while trying to return to Britain, and was extradited to Singapore, where he was tried, convicted, and sentenced to several years in prison.

Leeson's later life added a strange coda. He served his sentence in Singapore (during which he was diagnosed with cancer, which he survived), wrote a memoir, Rogue Trader, that was made into a film, and went on to a curious second career giving talks and even, for a time, working in finance and football administration — a transformation of the man who broke a bank into something close to a celebrity. The relative ease of that rehabilitation struck some as troubling, a sign of how the "rogue trader" can become a figure of fascination rather than simple condemnation. But the more important legacy was not personal: it was the permanent mark the collapse left on how banks are run. "Barings" became shorthand, in finance and risk management, for the catastrophe that follows when controls fail — a one-word warning taught to every new generation of bankers and regulators about the price of trusting without watching.

What is established, and what it means

The facts of the Barings collapse are thoroughly documented, including by official inquiries into how it happened. The lessons are foundational to modern risk management, and they are not really about one rogue individual at all.

The first and most important is the absolute necessity of separating duties. The single failure that made the disaster possible was letting Leeson control both the trading and the settlement of his own trades, which removed the independent check that exists precisely to stop a trader from concealing what they are doing. After Barings, the separation of front-office (trading) and back-office (settlement and control) functions became an iron rule of financial institutions, and the case is taught everywhere as the definitive illustration of why. A trader who can mark their own homework is a catastrophe waiting to happen, no matter how honest they seem or how solid the institution.

The second is the danger of unquestioned profits. Barings' management celebrated Leeson's apparent earnings without ever seriously asking how a single desk in Singapore could generate such large and consistent profits from relatively simple arbitrage trading. Genuine, large profits that seem to come too easily and that no one fully understands should provoke scrutiny, not just delight — because they may not be real, or may be the product of hidden, enormous risk. The same incuriosity about suspiciously good results that protected Madoff protected Leeson: people are reluctant to interrogate a golden goose.

In the end, Barings is the story of how fragile even the most venerable institution can be when its defences are hollow. A bank that had financed empires and outlasted Napoleon was destroyed in days by a 28-year-old trader with a secret account and a bad bet, and the earthquake that finished it was almost incidental — the losses were already mortal before the ground shook in Kobe. The lasting image is the note Leeson left behind, "I'm sorry," and the absurd, devastating fact that one of the great names of British finance was sold, at the end, for a single pound. It taught the financial world a lesson it has had to relearn periodically ever since: that no reputation is a substitute for control, that profits no one understands are a warning and not a triumph, and that an institution which lets one unwatched person take unlimited risk has already, whether it knows it or not, signed its own potential death warrant. Barings trusted, and did not watch, and 233 years ended with two words and a pound.

Sources

- The Bank of England's Board of Banking Supervision report on the collapse of Barings (1995) — primary.

- The Singapore inquiry and the court records of Nick Leeson's prosecution — primary.

- Nick Leeson, Rogue Trader (1996) — primary/secondary.

- Stephen Fay, The Collapse of Barings (1996) — secondary.

- Reporting by the Financial Times, the BBC, and others on the collapse and its aftermath (1995) — secondary.

- Rogue Trader (film, dir. James Dearden, 1999) — secondary.

- Analyses of the Barings case in risk-management and finance literature — academic.

Inspired this / based on it

Nick Leeson

Little, Brown. Leeson's own account, adapted into a 1999 film with Ewan McGregor.

James Dearden

Dramatization of the Barings collapse, starring Ewan McGregor as Leeson.

Stephen Fay

Richard Cohen Books. A detailed account of the bank's destruction.

Filed under

- #barings-leeson

- #nick-leeson

- #rogue-trader

- #fraud

- #singapore

- #futures-trading

- #barings-bank

- #kobe-earthquake

- #1990s

- #confirmed

Click any tag for every article carrying it.

Continue reading

Enron and the Most Innovative Company That Never Really Made Money

For six consecutive years, Fortune magazine named Enron the most innovative company in America. The Houston-based energy company had, the story went, transformed itself from a sleepy operator of natural-gas pipelines into a dazzling new kind of business — a trading powerhouse that bought and sold energy and almost anything else, light on physical assets and heavy on financial genius, the very model of the modern corporation. Its stock soared; its executives were celebrated as visionaries; its revenues, on paper, rocketed past $100 billion. And then, in the autumn of 2001, it all came apart with breathtaking speed. It emerged that Enron's reported profits were substantially an illusion, manufactured through aggressive and deceptive accounting; that the company had hidden enormous debts and losses in a web of hundreds of secretive off-the-books entities, some named after Star Wars characters; and that the 'innovation' the world had admired was, to a damaging degree, the art of making a company that did not really make money look as though it made a great deal. In about six weeks, Enron went from a $60 billion blue-chip giant to the largest corporate bankruptcy in American history to that point. Twenty thousand employees lost their jobs and, in many cases, their retirement savings, which had been tied up in Enron stock. Its auditor, Arthur Andersen — one of the five great global accounting firms — was destroyed in the fallout. The scandal sent executives to prison, prompted landmark reforms, and became the defining symbol of corporate fraud at the turn of the millennium. This article tells the story of how the most admired company in America turned out to be a confidence trick, and how the trick unravelled.

Wirecard and the €1.9 Billion That Never Existed

For years, Wirecard was a German success story almost too good to question. A digital-payments processor based outside Munich, it had risen from obscurity to become one of the most valuable companies in the country — admitted in 2018 to the DAX, the index of Germany's thirty biggest blue-chip firms, replacing a venerable bank. It was hailed as proof that Germany, too, could produce a world-beating technology champion, a fintech to rival Silicon Valley, and its share price soared to give it a value of around 24 billion euros. There was only one problem, and it was a fatal one: a large part of the company was fiction. In June 2020, Wirecard was forced to admit that 1.9 billion euros it claimed to be holding in trustee accounts in Asia — a sum representing the bulk of its supposed profits — could not be found, and, in the company's own startling words, probably did not exist. The admission detonated one of the largest accounting frauds in modern European history. The company collapsed into insolvency within days; its chief executive was arrested; and its chief operating officer, Jan Marsalek, vanished, fleeing the country and surfacing in the orbit of Russian intelligence. The most damning part was that the alarm had been sounding for years: the Financial Times, in a long and lonely investigation, had reported again and again that Wirecard's numbers did not add up — only to be attacked, sued, and investigated itself, while German regulators went after the journalists and short-sellers rather than the company. This article tells the story of the money that never existed, the reporters who refused to let it go, and how a country's pride blinded it to a fraud in plain sight.

Bernie Madoff and the Biggest Ponzi Scheme in History

Bernard L. Madoff was not a fringe hustler but a pillar of Wall Street. He had helped build the Nasdaq stock market and served as its chairman; he ran a respected market-making firm; he moved easily among the wealthy, the philanthropic, and the powerful. And alongside his legitimate business, he ran an investment-advisory operation that was, for decades, the envy of finance: a fund that delivered remarkably steady, positive returns year after year, in good markets and bad, never seeming to lose money. To be allowed to invest with Madoff was a mark of status, a privilege extended to wealthy individuals, charities, university endowments, banks, and feeder funds around the world. There was only one problem, and it was total: the investments did not exist. Madoff was not generating those steady returns by any strategy at all. He was running a Ponzi scheme — paying the 'returns' and redemptions of existing investors with the fresh money of new ones, while no real trading took place. For decades it worked, because as long as more money came in than went out, the scheme could continue and the statements could show whatever Madoff wanted them to show. When the financial crisis of 2008 triggered a wave of withdrawals he could not meet, the scheme collapsed, and the scale of it stunned the world: customer account statements showed about $65 billion that did not exist, built on perhaps $17–20 billion of real money that investors had actually handed over and that was now largely gone. It was the largest Ponzi scheme in history. And the most damning detail of all was that a financial analyst named Harry Markopolos had been telling the Securities and Exchange Commission, repeatedly and in detail, for nine years, that Madoff was a fraud — and had been ignored. This article tells the story of the respectable man who ran the biggest financial fraud ever, the warnings the watchdogs missed, and the lives it destroyed.