Category

Finance & Economy

Panama Papers, LIBOR, FTX. Where money moves in the dark.

13 articles

Nick Leeson and the Rogue Trader Who Broke a 233-Year-Old Bank

Barings Bank was an institution almost synonymous with British financial respectability. Founded in 1762, it had financed the Napoleonic Wars and the Louisiana Purchase, served the British monarchy, and survived for 233 years as one of the City of London's most venerable merchant banks. In February 1995, it ceased to exist — destroyed not by war or recession but by a single trader on the other side of the world. Nick Leeson, a 28-year-old from a working-class background, ran Barings' futures-trading operation in Singapore, and he appeared to be a star, generating spectacular profits that made him one of the bank's most valued employees. In reality, he was concealing catastrophic losses in a secret error account numbered 88888, doubling down again and again on losing bets that the Japanese stock market would stay stable. The bank's management, dazzled by his apparent success and failing utterly to supervise him, kept sending him money to cover his positions, believing it was funding profitable trades. Then, on 17 January 1995, a massive earthquake struck the Japanese city of Kobe, sending the Tokyo market into turmoil and turning Leeson's enormous bets disastrously wrong. As the losses ballooned past the bank's entire capital — ultimately around £827 million — Leeson fled, leaving a note that read 'I'm sorry.' Within days, Barings was bankrupt, sold to a Dutch bank for one pound. This article tells the story of how one unsupervised young man, a hidden account, and an earthquake brought down a bank that had stood for nearly two and a half centuries — and what it revealed about the dangers of trading without control.

Bre-X and the Biggest Gold Discovery That Never Existed

In the mid-1990s, a small, obscure Canadian exploration company called Bre-X Minerals announced that it had found something extraordinary in the jungles of Borneo: a gold deposit at a site called Busang, in the Indonesian province of East Kalimantan, that appeared to be one of the largest in the history of the world. As the company drilled and reported ever more spectacular results — tens of millions of ounces of gold, then more, then more still, eventually an estimated 70 million ounces or beyond — a frenzy took hold. Bre-X's stock, which had once traded for pennies, rocketed upward, at its peak valuing the company at around six billion Canadian dollars. Ordinary investors, pension funds, and mining giants alike scrambled to get a piece of the find of the century; the government of Indonesia and powerful interests jockeyed for control of the riches. There was only one problem, and it was as complete as a fraud can be: there was essentially no gold. The astonishing drilling results had been faked, the rock samples salted by hand with gold dust — much of it, it was later determined, panned from rivers or bought, sprinkled into the crushed core samples to simulate a deposit that did not exist. When a rival company's careful testing finally exposed the truth in 1997, Bre-X collapsed to nothing, vaporising billions of dollars. And at the centre of the unravelling, the company's chief geologist, Michael de Guzman, fell to his death from a helicopter over the Borneo jungle — a death officially ruled suicide but shrouded, like the whole affair, in lasting mystery. This article tells the story of the largest mining fraud in history: the gold that was never there, the salting that created it, and the fortune that vanished into the rainforest.

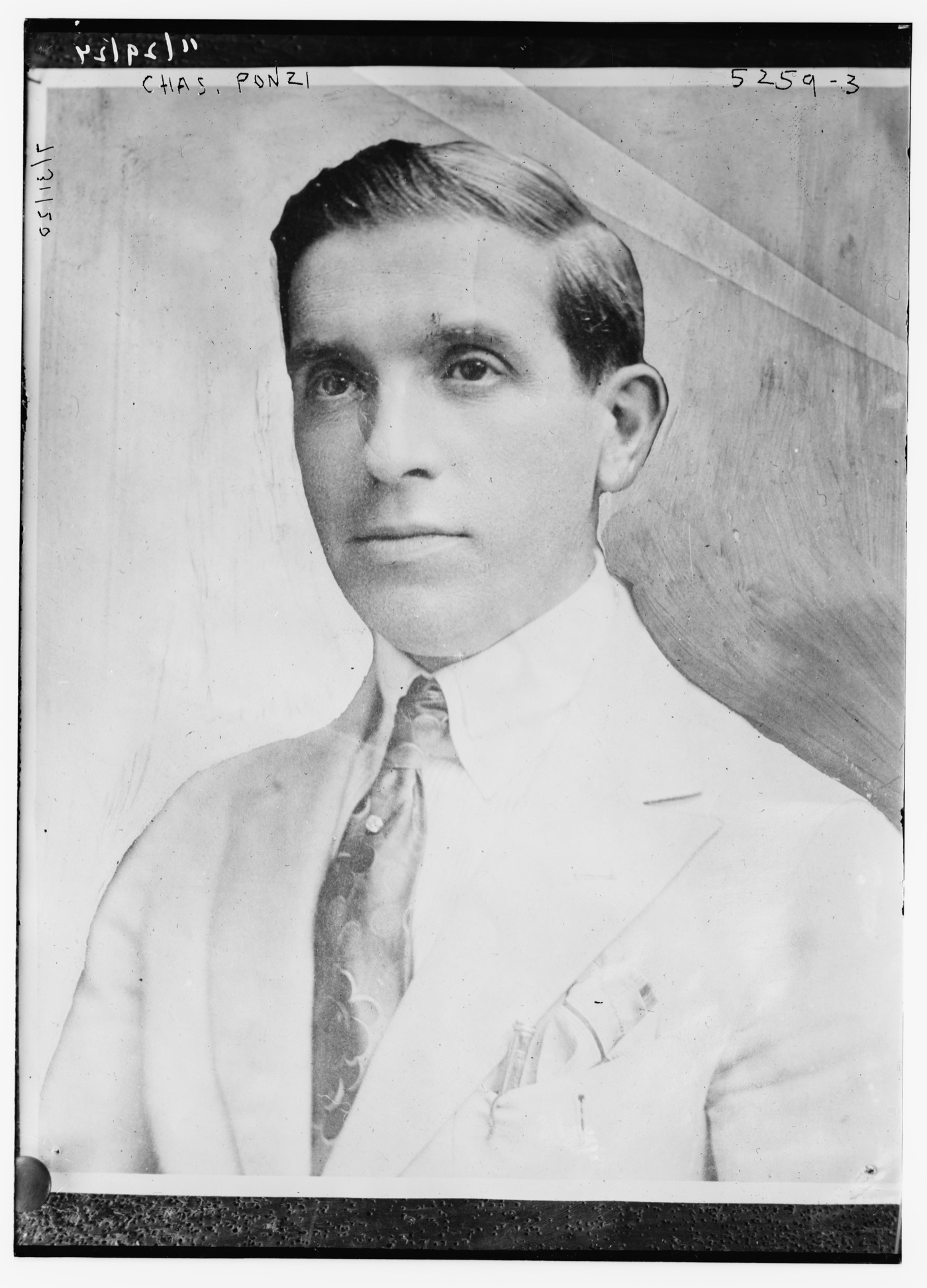

Charles Ponzi and the Scheme That Bears His Name

In the summer of 1920, a small, dapper Italian immigrant named Charles Ponzi was the most talked-about man in Boston. From a modest office on School Street, he was offering something that sounded impossible and turned out to be exactly that: a 50 percent return in 45 days, a 100 percent return in 90 days, on an investment he said was backed by a clever arbitrage in international postal reply coupons. Money poured in — from labourers and police officers, from widows and shopkeepers, from people who mortgaged their homes and emptied their savings to get a piece of it. At the height of the mania he was taking in hundreds of thousands of dollars a day, and crowds lined up outside his door pressing cash into his hands. The arbitrage he described was real in theory and worthless in practice; the coupons were never traded in any meaningful volume. What Ponzi was actually doing was paying his early investors with the money of his later ones — sustaining the illusion of fabulous profits only as long as new money flowed in faster than old money was withdrawn. It could not last, and it did not. Within months a newspaper, a financial analyst, and a disillusioned publicity man had pulled the structure apart, a run emptied his company, and an audit revealed that behind the millions he had collected there was nothing but debt. He went to prison, was deported, and died penniless in a charity ward in Rio de Janeiro. But his name did not die with him: the confidence trick he performed so memorably — paying old investors with new investors' money and calling it profit — has been known ever since as the Ponzi scheme. This is the story of the man behind the name.

WorldCom and the $11 Billion Accounting Fraud

By the turn of the millennium, WorldCom was one of the largest telecommunications companies on earth — a sprawling empire assembled in barely a decade by a former milkman and basketball coach named Bernard Ebbers, who had bought up dozens of rivals to turn a tiny Mississippi long-distance reseller into a colossus that carried a huge share of the world's internet traffic and owned the famous MCI brand. Then the telecom bubble burst, revenues sagged, and the company faced an impossible problem: how to keep reporting the steady profits that Wall Street demanded when the underlying business was deteriorating. The answer, devised by its finance department, was breathtakingly simple and entirely fraudulent. Ordinary operating expenses — the fees WorldCom paid other networks to carry its calls — were quietly reclassified as long-term capital investments, the way a company might treat the cost of building a factory. With a few accounting entries, billions of dollars in costs vanished from the books and reappeared as assets, and the losses turned, on paper, into healthy profits. The deception eventually totalled some $11 billion, the largest accounting fraud yet seen. It was uncovered not by regulators or outside auditors but by WorldCom's own internal-audit team — a handful of people led by a vice-president named Cynthia Cooper, who pursued the anomalies in secret, often at night, against the resistance of the company's own chief financial officer. When they brought their findings to the board in June 2002, the company collapsed into the biggest bankruptcy in American history, its CEO was sent to prison for twenty-five years, and Congress passed a sweeping law that changed how every public company in the country keeps its books. This is the story of the fraud, the woman who exposed it, and the reckoning that followed.

Enron and the Most Innovative Company That Never Really Made Money

For six consecutive years, Fortune magazine named Enron the most innovative company in America. The Houston-based energy company had, the story went, transformed itself from a sleepy operator of natural-gas pipelines into a dazzling new kind of business — a trading powerhouse that bought and sold energy and almost anything else, light on physical assets and heavy on financial genius, the very model of the modern corporation. Its stock soared; its executives were celebrated as visionaries; its revenues, on paper, rocketed past $100 billion. And then, in the autumn of 2001, it all came apart with breathtaking speed. It emerged that Enron's reported profits were substantially an illusion, manufactured through aggressive and deceptive accounting; that the company had hidden enormous debts and losses in a web of hundreds of secretive off-the-books entities, some named after Star Wars characters; and that the 'innovation' the world had admired was, to a damaging degree, the art of making a company that did not really make money look as though it made a great deal. In about six weeks, Enron went from a $60 billion blue-chip giant to the largest corporate bankruptcy in American history to that point. Twenty thousand employees lost their jobs and, in many cases, their retirement savings, which had been tied up in Enron stock. Its auditor, Arthur Andersen — one of the five great global accounting firms — was destroyed in the fallout. The scandal sent executives to prison, prompted landmark reforms, and became the defining symbol of corporate fraud at the turn of the millennium. This article tells the story of how the most admired company in America turned out to be a confidence trick, and how the trick unravelled.

FTX and the Crypto King Who Gambled With Other People's Money

Sam Bankman-Fried looked nothing like a master of the financial universe, and that was part of the appeal. He slept on a beanbag, wore cargo shorts and a rumpled T-shirt to meetings with the most powerful investors in the world, played video games while pitching them, and let his hair grow into a famous unruly mop. He talked not about getting rich but about giving it all away — a devotee of 'effective altruism,' the philosophy of earning as much as possible in order to donate it to causes that do the most good. By 2022 his cryptocurrency exchange, FTX, was valued at around $32 billion, one of the largest in the world; his face was on a Miami sports arena and a Super Bowl commercial; he had become the acceptable, philanthropic face of a chaotic crypto industry, courted by celebrities, politicians, and regulators alike. And then, over about ten days in November 2022, the whole edifice collapsed with stunning speed. It emerged that roughly $8 billion of FTX customers' money was simply gone — that the exchange had secretly funnelled its customers' deposits to Bankman-Fried's affiliated hedge fund, Alameda Research, which had gambled and lost much of it. There was no sophisticated technology failure and no clever scheme that merely went wrong; a court would find it was straightforward fraud and theft on an enormous scale. Bankman-Fried was arrested, tried, convicted on all counts, and in 2024 sentenced to 25 years in prison. This article tells the story of how a young man in shorts became the king of crypto, how he stole billions while presenting himself as the industry's most ethical figure, and how it all came apart in less than two weeks.

Bernie Madoff and the Biggest Ponzi Scheme in History

Bernard L. Madoff was not a fringe hustler but a pillar of Wall Street. He had helped build the Nasdaq stock market and served as its chairman; he ran a respected market-making firm; he moved easily among the wealthy, the philanthropic, and the powerful. And alongside his legitimate business, he ran an investment-advisory operation that was, for decades, the envy of finance: a fund that delivered remarkably steady, positive returns year after year, in good markets and bad, never seeming to lose money. To be allowed to invest with Madoff was a mark of status, a privilege extended to wealthy individuals, charities, university endowments, banks, and feeder funds around the world. There was only one problem, and it was total: the investments did not exist. Madoff was not generating those steady returns by any strategy at all. He was running a Ponzi scheme — paying the 'returns' and redemptions of existing investors with the fresh money of new ones, while no real trading took place. For decades it worked, because as long as more money came in than went out, the scheme could continue and the statements could show whatever Madoff wanted them to show. When the financial crisis of 2008 triggered a wave of withdrawals he could not meet, the scheme collapsed, and the scale of it stunned the world: customer account statements showed about $65 billion that did not exist, built on perhaps $17–20 billion of real money that investors had actually handed over and that was now largely gone. It was the largest Ponzi scheme in history. And the most damning detail of all was that a financial analyst named Harry Markopolos had been telling the Securities and Exchange Commission, repeatedly and in detail, for nine years, that Madoff was a fraud — and had been ignored. This article tells the story of the respectable man who ran the biggest financial fraud ever, the warnings the watchdogs missed, and the lives it destroyed.

Nikola and the Electric Truck That Rolled Downhill

In June 2020, an electric-and-hydrogen truck company called Nikola went public, and within days its stock-market value briefly soared past that of Ford — the hundred-and-seventeen-year-old maker of millions of actual vehicles. Nikola, by contrast, had never sold a single truck, never produced one for a paying customer, and had essentially no revenue. What it had was a vision — zero-emission semi-trucks powered by batteries and hydrogen fuel cells that would clean up the heavily polluting world of long-haul freight — and a charismatic founder, Trevor Milton, who sold that vision with relentless, theatrical confidence. He named the company after Nikola Tesla (the electric-car company Tesla having taken the inventor's surname), positioned himself as the next Elon Musk, and made a stream of bold claims about trucks that worked, technology that was ready, and orders worth billions. The most famous demonstration of Nikola's prototype showed one of its trucks gliding smoothly along a road, apparently under its own power — proof, it seemed, that the vehicle was real and functional. It was not. The truck had no working powertrain; it had simply been towed to the top of a gentle hill and allowed to roll down under gravity, filmed so as to look as if it were driving. When a short-seller's report revealed this and a litany of other deceptions in September 2020, Nikola's story began to collapse. Trevor Milton was charged with fraud, and in 2023 he was convicted. This article tells the story of the truck that rolled downhill — a case study in how far hype, a green mission, and a confident founder could inflate a company built on claims that were not true.

uBiome and the Gut-Test Startup That Billed Its Way to a Billion

uBiome arrived with one of the most appealing pitches of the health-technology boom: that by sequencing the trillions of microbes living in your gut — your microbiome — it could unlock insights into your health, from digestion to mood to disease, and put the power of cutting-edge genomics into the hands of ordinary consumers. Founded in San Francisco in 2012, it rode a genuine wave of scientific excitement about the microbiome, raised tens of millions of dollars from prominent venture capitalists, was hailed as a rising star of the gut-health revolution, and reached a valuation approaching a billion dollars. But beneath the science-forward image was a business model that, federal prosecutors would allege, was substantially a fraud — not in the technology so much as in the billing. To turn its consumer curiosity-kit into real revenue, uBiome had pushed its tests into the medical system and billed health insurers aggressively and improperly for them: ordering tests that were not medically necessary, billing for the same samples more than once, and using doctors who were not genuinely independent to authorise the orders. The company's revenue, the case suggested, came less from a breakthrough in health than from a scheme to extract money from insurers. In April 2019 the FBI raided uBiome's offices; the founders were placed on leave and then departed; the company filed for bankruptcy within months; and the two co-founders were ultimately charged with fraud. This article tells the story of uBiome — a quieter, more technical cautionary tale than its famous cousins, but in some ways a more revealing one, because its fraud was hidden not in a fake machine or a missing billion but in the mundane, lucrative mechanics of medical billing.

WeWork and the $47 Billion Office Company That Wasn't a Tech Company

Adam Neumann walked barefoot through New York, flew on a private jet stocked with tequila and marijuana, and told people he intended to become the world's first trillionaire, to live forever, to solve the problem of homelessness, and to 'elevate the world's consciousness.' His company, WeWork, was — when you stripped away the mysticism — a business that signed long-term leases on office buildings, fitted them out with exposed brick, free beer, and communal sofas, and rented the space back to startups and freelancers on short-term, flexible terms. It was, in plain terms, a commercial real-estate company. But Neumann did not sell it as one. He sold WeWork as a technology company, a community, a movement, a 'physical social network' that would transform how people worked and lived; and Silicon Valley, awash in cheap money and hungry for the next world-changing platform, believed him. Backed above all by the Japanese conglomerate SoftBank, WeWork reached a private valuation of about $47 billion by early 2019, making it one of the most valuable startups in the world. Then, in the late summer of 2019, the company filed the paperwork to go public — and the spell broke. Investors and journalists read the prospectus and found enormous losses, an unsustainable business model, bizarre self-dealing by the founder, and governance so lopsided it bordered on absurd. In about six weeks, WeWork's valuation cratered from $47 billion toward single-digit billions, the public offering was abandoned, and Neumann was pushed out. Unlike some of its fellow cautionary tales, WeWork was not a criminal fraud — no one went to prison. It was something subtler and, in its way, more revealing: a legal, dazzling demonstration of how cheap money and a magnetic founder can inflate a fairly ordinary business into a fantasy, and how fast the fantasy can pop. This is the story of how that happened.

Wirecard and the €1.9 Billion That Never Existed

For years, Wirecard was a German success story almost too good to question. A digital-payments processor based outside Munich, it had risen from obscurity to become one of the most valuable companies in the country — admitted in 2018 to the DAX, the index of Germany's thirty biggest blue-chip firms, replacing a venerable bank. It was hailed as proof that Germany, too, could produce a world-beating technology champion, a fintech to rival Silicon Valley, and its share price soared to give it a value of around 24 billion euros. There was only one problem, and it was a fatal one: a large part of the company was fiction. In June 2020, Wirecard was forced to admit that 1.9 billion euros it claimed to be holding in trustee accounts in Asia — a sum representing the bulk of its supposed profits — could not be found, and, in the company's own startling words, probably did not exist. The admission detonated one of the largest accounting frauds in modern European history. The company collapsed into insolvency within days; its chief executive was arrested; and its chief operating officer, Jan Marsalek, vanished, fleeing the country and surfacing in the orbit of Russian intelligence. The most damning part was that the alarm had been sounding for years: the Financial Times, in a long and lonely investigation, had reported again and again that Wirecard's numbers did not add up — only to be attacked, sued, and investigated itself, while German regulators went after the journalists and short-sellers rather than the company. This article tells the story of the money that never existed, the reporters who refused to let it go, and how a country's pride blinded it to a fraud in plain sight.

The Bofors Scandal and the Bribes That Felled a Government

In March 1986, the Swedish arms manufacturer Bofors signed the contract of its life: a deal worth around 1.3 billion US dollars to supply 410 field howitzers to the army of India, beating its rivals for one of the largest defence orders of the decade. A little over a year later, in April 1987, Swedish public radio broadcast a revelation that would turn the triumph into one of the most consequential corruption scandals in the history of either country: to win the contract, Bofors had paid roughly 64 million dollars in secret commissions — bribes, in plain terms — funnelled through a web of front companies and secret Swiss bank accounts, in direct violation of India's rules forbidding middlemen and payoffs in defence deals. The question that consumed India for the next two decades was simple and explosive: who received the money? The investigation led through coded Swiss accounts to a circle of intermediaries, and above all to an Italian businessman, Ottavio Quattrocchi, who was personally close to the family of India's prime minister, Rajiv Gandhi. The scandal became a weapon in Indian politics, a symbol of corruption at the highest level, and a central reason Gandhi's government was swept from power in the 1989 election. Yet for all the decades of investigation that followed — across India, Sweden, and Switzerland — almost no one was ever convicted, the key suspect was never extradited, and the precise truth of who pocketed the bribes was never fully established in a court of law. This article sets out what is firmly known about the Bofors affair, what remains contested, and why a Swedish weapons deal became the scandal that would not die.