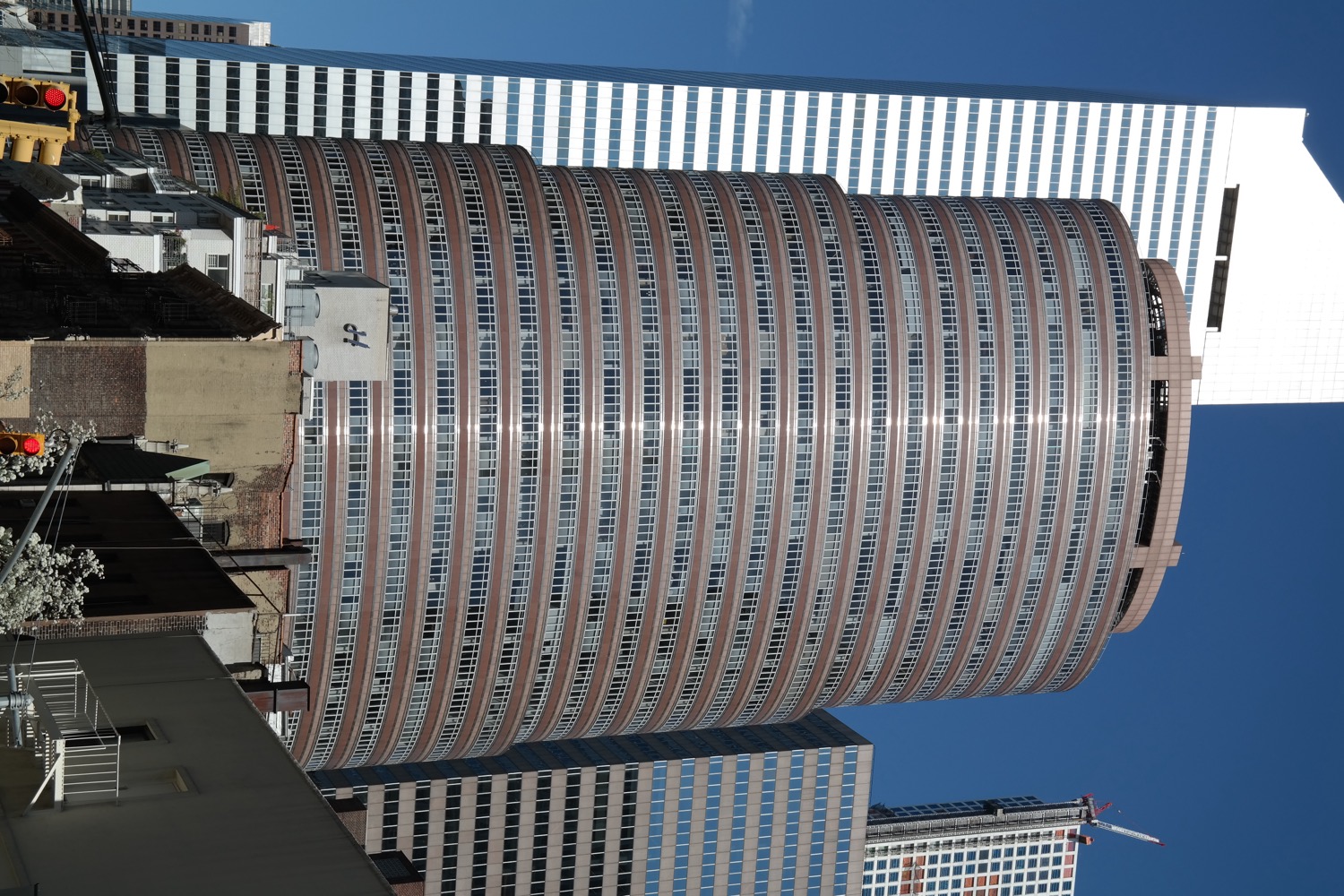

The Lipstick Building in Midtown Manhattan, where Bernard Madoff's firm occupied several floors. From this respectable address, on a separate, secretive floor, Madoff ran the largest Ponzi scheme in history for decades — paying old investors with new investors' money while no real trading took place. Wikimedia Commons / Choinowski, CC BY-SA 4.0.

Bernie Madoff and the Biggest Ponzi Scheme in History

United States, 1960s–2008 — Bernie Madoff was a Wall Street eminence, a former Nasdaq chairman whose investment fund delivered steady, beautiful returns for decades. There were no investments. It was a Ponzi scheme, the largest ever — and one analyst had been warning the regulators for nine years

- Category

- Finance & Economy

- Published

- Length

- 4,060 words · 19 min read

- Author

- The editors

The Madoff scandal is the purest example in this archive of a fraud protected by respectability. Unlike a flashy startup or a high-flying new company, Madoff's operation drew its power from the opposite of novelty — from his decades of Wall Street eminence, his establishment credentials, his reputation as a sober, trustworthy elder of finance. The fraud worked not despite his respectability but because of it: who would suspect the former chairman of Nasdaq, the man whose name opened every door, of running a common confidence trick? Madoff is the reminder that the most dangerous frauds are not always the brashest, but sometimes the quietest and most trusted.

This is the story of the biggest Ponzi scheme in history.

The respectable fraud

Everything about Bernie Madoff signalled trustworthiness. He had founded his firm, Bernard L. Madoff Investment Securities, in 1960, and built it into a significant and legitimate market-making business — a firm that helped match buyers and sellers of stocks and was, for a time, a real innovator in electronic trading. He served as chairman of Nasdaq, the electronic stock market, putting him at the very heart of the financial establishment. He was wealthy, philanthropic, and well-connected, active in Jewish charitable circles and trusted implicitly by the people around him. He did not promise outlandish riches or pressure people to invest; on the contrary, access to his fund was made to feel exclusive, a quiet privilege for those fortunate enough to be let in.

This respectability was the foundation of the fraud. Investors trusted Madoff because of who he was, and that trust substituted for the scrutiny they might otherwise have applied. Feeder funds — investment funds whose whole purpose was to channel clients' money to Madoff — sprang up, and through them his reach extended across the world, to banks and funds and wealthy families on multiple continents, many of whom did not even know that Madoff was the ultimate destination of their money. The respectable name at the centre reassured everyone, and the reassurance spread outward through the network until tens of billions of dollars had flowed in.

The returns that were too good to be true

The bait was the performance. Madoff's fund reported remarkably consistent positive returns — not spectacular, get-rich-quick numbers, which might have aroused suspicion, but steady, solid gains, year after year, that almost never wavered and almost never showed a losing period, regardless of whether the broader market was booming or crashing. He attributed this to a plausible-sounding investment strategy (a so-called "split-strike conversion" involving stocks and options). For investors, this consistency was intoxicating: a fund that just kept going up, smoothly, through every kind of market, was the holy grail of investing.

But that very consistency was, to anyone who understood markets, deeply suspicious — indeed impossible. Real investment returns are volatile; markets go up and down, and any genuine strategy has good years and bad, winning months and losing ones. A fund that delivered steady positive returns through booms, busts, and crashes, almost never losing, was not displaying skill — it was displaying something that does not occur in nature. The smoothness that delighted the investors was precisely the red flag that should have alerted the experts, because it implied either a risk-free money machine, which does not exist, or fabrication. The numbers were too good to be true in the most literal sense: they were not true.

How the Ponzi worked

The mechanism behind the beautiful returns was the oldest financial fraud there is, named for Charles Ponzi, who ran a famous version in 1920. In a Ponzi scheme, there is no real investment generating returns; instead, the operator pays the "profits" and withdrawals of existing investors using the money deposited by new investors. As long as new money keeps flowing in faster than old money is withdrawn, the scheme can continue indefinitely, and each investor who checks their account sees healthy, growing balances — balances that are pure fiction, mere numbers on a statement, backed by no actual assets.

Madoff's version was a Ponzi scheme on an unprecedented scale and of unusual longevity. Behind the legitimate market-making business, on a separate and secretive floor of his office in the Lipstick Building, his advisory operation simply took in investors' money and did not invest it. The steady returns on the statements were invented; when investors wanted to withdraw, they were paid from the pool of incoming funds. The fabricated account statements and trade confirmations were generated to support the illusion, showing trades that had never happened. For as long as Madoff could keep attracting new money and most investors left their balances in place (lured by the wonderful returns), the scheme could roll on. And it rolled on for a very long time — by most accounts for decades.

A peculiar feature of Madoff's operation, and part of why it eluded detection, was its split nature. His firm had a large, legitimate, and well-regarded market-making business, employing many people who had no idea anything was wrong, occupying floors of the Lipstick Building in full public view. The Ponzi scheme ran separately, on its own floor, with its own small and intensely loyal staff, walled off from the legitimate operation. This structure provided both camouflage and credibility: the real business lent the fraudulent one an air of substance, and the secrecy of the advisory operation — Madoff was famously opaque about how he generated his returns, framing it as protecting a proprietary edge — discouraged the questions that might have exposed it. A wholly fake company invites scrutiny; a real and respected company with a hidden fraudulent annex is far harder to see through.

The longevity also meant that, by the end, the fabricated wealth had compounded into staggering, and entirely fictional, sums. Investors who had been with Madoff for years or decades saw their statements show balances that had grown enormously, and many treated those numbers as real wealth — spending against them, planning retirements around them, leaving them to heirs. The cruelty of a long-running Ponzi is that the longer it lasts, the more devastating its collapse, because the victims have come to believe ever more completely in money that was never there. When Madoff fell, people discovered not only that their recent gains were illusory but that, in many cases, the entire fortune they thought they had accumulated over a lifetime had never existed at all.

The warnings that were ignored

The most scandalous aspect of the Madoff affair — the part that makes it a story of institutional failure and not just individual crime — is that the fraud was detected, repeatedly, by someone who tried hard to stop it, and that the authorities did nothing. Harry Markopolos, a financial analyst with expertise in the kind of strategy Madoff claimed to use, became convinced as early as 2000 that Madoff's returns were mathematically impossible and that he was running a Ponzi scheme. Markopolos did the analysis, showed that the numbers could not be real, and submitted his findings to the Securities and Exchange Commission — the federal regulator responsible for policing exactly this kind of fraud.

He did this not once but repeatedly, over roughly nine years, in increasingly detailed and urgent submissions, at one point laying out his case in a document pointedly titled "The World's Largest Hedge Fund Is a Fraud." He was not a lone crank; his analysis was rigorous, and he was so convinced of Madoff's criminality, and so frustrated by the inaction, that he reportedly feared for his own safety. And yet the SEC, despite these warnings, despite conducting some examinations of Madoff, failed to uncover the fraud. The regulator looked and did not see, deterred perhaps by Madoff's stature, hampered by inexperience and a failure to grasp what Markopolos was telling them, and unwilling to believe that so eminent a figure could be a criminal. For nine years, the watchdog was handed the answer and could not act on it.

The collapse

What finally killed the scheme was not the regulators but the market. The financial crisis of 2008 changed the flow of money: as markets crashed and investors everywhere scrambled for cash, Madoff's clients began asking to withdraw their funds on a scale he could not meet. With redemption requests reportedly reaching billions of dollars and new money drying up, the fundamental vulnerability of every Ponzi scheme — its dependence on inflows exceeding outflows — became fatal. There was no real pool of assets to draw on, because there had never been any real investing; the money simply was not there.

In December 2008, with the scheme about to be exposed by his inability to pay, Bernie Madoff confessed — reportedly first to his sons, who turned him in to the authorities. He was arrested, and the scale of the fraud became public. The account statements of his roughly thousands of clients reflected about $65 billion in holdings; the actual amount of real money that investors had put in and lost was estimated at something like $17 to $20 billion. Either way, it was the largest Ponzi scheme ever uncovered, dwarfing all predecessors. A man at the summit of financial respectability was revealed as the perpetrator of history's biggest investment fraud.

The victims

The human cost of the Madoff fraud was vast and varied. Because his investors included not just the wealthy but charities, foundations, pension funds, and ordinary people who had entrusted him with their life savings (often through feeder funds), the collapse devastated a wide range of lives. Some charitable foundations were wiped out and forced to close. Universities and institutions lost endowment money. Individual investors — including elderly retirees who had believed their money was safe with the trustworthy Mr. Madoff — lost everything, their financial security erased in an instant. Among the famous victims were the Nobel laureate and Holocaust survivor Elie Wiesel and his foundation, which lost much of its assets. The betrayal was especially bitter because so many of the victims had trusted Madoff personally, as a respected member of their own communities.

The suffering extended into tragedy. The stress and ruin drove some connected to the affair to despair; Madoff's own son Mark later died by suicide, on the second anniversary of his father's arrest. The fraud did not merely destroy fortunes; it shattered lives, families, and institutions, and the human wreckage was as much a part of its scale as the dollar figures.

The reckoning

The legal resolution was swift and severe. Bernie Madoff pleaded guilty in March 2009 to multiple felonies and, in June 2009, was sentenced to 150 years in prison — a symbolic term reflecting the enormity of his crimes, ensuring he would die behind bars. He did, in 2021. A court-appointed trustee, Irving Picard, undertook a years-long effort to recover money for the victims, suing those who had withdrawn more than they put in and pursuing the banks and feeder funds connected to the scheme. This recovery effort was, over time, remarkably successful in financial terms, ultimately returning a large fraction of the real money lost to the victims — though no recovery could undo the years of fear, ruin, and grief.

The SEC, humiliated by its failure to act on Markopolos's warnings, undertook internal reviews and reforms. Markopolos himself testified before Congress, becoming a symbol of the diligent outsider whom the system had ignored, and his account of the affair (later a book) was a devastating indictment of regulatory failure. The case prompted soul- searching about how the watchdogs could have been handed the solution to the largest fraud in history and still missed it for the better part of a decade.

What is established, and what it means

The facts of Madoff are entirely settled by his guilty plea, the trustee's accounting, and exhaustive investigation. The lessons are fundamental, and they recur throughout the study of fraud.

The first is the danger of trusting reputation over verification. Madoff got away with it for so long because he was respectable, and respectability disarmed scrutiny. His investors, his feeder funds, even the regulators substituted his eminence for due diligence — they trusted who he was instead of checking what he did. The lesson is that reputation, status, and the recommendation of trusted others are not evidence of honesty; they are exactly the cover that the most successful frauds rely on. The question "but how, precisely, are these returns generated?" should never be waived because the person being asked is important.

The second is the deadly significance of returns that are too consistent. Markopolos cracked the case essentially by noticing that Madoff's returns were impossibly smooth — that no genuine strategy produces steady gains through every market. This is a transferable warning: in investing, consistency that seems to defy the volatility of markets is not a sign of genius but a red flag for fraud. Real returns are bumpy; a line that only goes up, smoothly, forever, is usually a lie. The very feature that made Madoff's fund attractive was the feature that proved it false — if anyone chose to see it.

In the end, Madoff is the fraud that wore the face of trust. There was no clever new technology, no dazzling vision, no get-rich-quick promise — only the steady, reassuring returns of a respected man whom everyone believed, sustained by the oldest trick in finance and protected by the last thing anyone thought to question: his own good name. For decades it held, while an analyst shouted the truth at a regulator that would not listen, until the crisis of 2008 pulled away the new money the scheme depended on and revealed that behind the $65 billion in account statements there was, essentially, nothing. The biggest investment fraud in history was not the boldest or the most ingenious; it was the most trusted. And that is its enduring warning: that the safest-seeming proposition, vouched for by the most respectable people, can be the emptiest of all — and that no reputation, however gilded, is a substitute for asking where the money actually is.

Sources

- The criminal case United States v. Bernard L. Madoff (2009), his guilty plea and sentencing — primary.

- Harry Markopolos's submissions to the SEC, including "The World's Largest Hedge Fund Is a Fraud" (2005), and his congressional testimony — primary.

- The SEC Office of Inspector General report on the agency's failure to uncover the Madoff fraud (2009) — primary.

- The work and filings of the bankruptcy trustee, Irving Picard, on recovering assets for victims — primary.

- Harry Markopolos, No One Would Listen: A True Financial Thriller (2010) — secondary.

- Diana B. Henriques, The Wizard of Lies: Bernie Madoff and the Death of Trust (2011) — secondary.

- Reporting by The New York Times, The Wall Street Journal, and others on the collapse, the victims, and the recovery (2008–2021) — secondary.

Inspired this / based on it

Diana B. Henriques

Times Books. The definitive account; adapted into an HBO film (2017) with Robert De Niro.

Harry Markopolos

Wiley. The whistleblower's own account of warning the SEC for years.

Netflix

Documentary series on the scheme and its collapse.

Filed under

- #madoff-ponzi

- #bernie-madoff

- #ponzi-scheme

- #fraud

- #wall-street

- #harry-markopolos

- #sec

- #investment-fraud

- #2000s

- #confirmed

Click any tag for every article carrying it.

Continue reading

Charles Ponzi and the Scheme That Bears His Name

In the summer of 1920, a small, dapper Italian immigrant named Charles Ponzi was the most talked-about man in Boston. From a modest office on School Street, he was offering something that sounded impossible and turned out to be exactly that: a 50 percent return in 45 days, a 100 percent return in 90 days, on an investment he said was backed by a clever arbitrage in international postal reply coupons. Money poured in — from labourers and police officers, from widows and shopkeepers, from people who mortgaged their homes and emptied their savings to get a piece of it. At the height of the mania he was taking in hundreds of thousands of dollars a day, and crowds lined up outside his door pressing cash into his hands. The arbitrage he described was real in theory and worthless in practice; the coupons were never traded in any meaningful volume. What Ponzi was actually doing was paying his early investors with the money of his later ones — sustaining the illusion of fabulous profits only as long as new money flowed in faster than old money was withdrawn. It could not last, and it did not. Within months a newspaper, a financial analyst, and a disillusioned publicity man had pulled the structure apart, a run emptied his company, and an audit revealed that behind the millions he had collected there was nothing but debt. He went to prison, was deported, and died penniless in a charity ward in Rio de Janeiro. But his name did not die with him: the confidence trick he performed so memorably — paying old investors with new investors' money and calling it profit — has been known ever since as the Ponzi scheme. This is the story of the man behind the name.

Enron and the Most Innovative Company That Never Really Made Money

For six consecutive years, Fortune magazine named Enron the most innovative company in America. The Houston-based energy company had, the story went, transformed itself from a sleepy operator of natural-gas pipelines into a dazzling new kind of business — a trading powerhouse that bought and sold energy and almost anything else, light on physical assets and heavy on financial genius, the very model of the modern corporation. Its stock soared; its executives were celebrated as visionaries; its revenues, on paper, rocketed past $100 billion. And then, in the autumn of 2001, it all came apart with breathtaking speed. It emerged that Enron's reported profits were substantially an illusion, manufactured through aggressive and deceptive accounting; that the company had hidden enormous debts and losses in a web of hundreds of secretive off-the-books entities, some named after Star Wars characters; and that the 'innovation' the world had admired was, to a damaging degree, the art of making a company that did not really make money look as though it made a great deal. In about six weeks, Enron went from a $60 billion blue-chip giant to the largest corporate bankruptcy in American history to that point. Twenty thousand employees lost their jobs and, in many cases, their retirement savings, which had been tied up in Enron stock. Its auditor, Arthur Andersen — one of the five great global accounting firms — was destroyed in the fallout. The scandal sent executives to prison, prompted landmark reforms, and became the defining symbol of corporate fraud at the turn of the millennium. This article tells the story of how the most admired company in America turned out to be a confidence trick, and how the trick unravelled.

FTX and the Crypto King Who Gambled With Other People's Money

Sam Bankman-Fried looked nothing like a master of the financial universe, and that was part of the appeal. He slept on a beanbag, wore cargo shorts and a rumpled T-shirt to meetings with the most powerful investors in the world, played video games while pitching them, and let his hair grow into a famous unruly mop. He talked not about getting rich but about giving it all away — a devotee of 'effective altruism,' the philosophy of earning as much as possible in order to donate it to causes that do the most good. By 2022 his cryptocurrency exchange, FTX, was valued at around $32 billion, one of the largest in the world; his face was on a Miami sports arena and a Super Bowl commercial; he had become the acceptable, philanthropic face of a chaotic crypto industry, courted by celebrities, politicians, and regulators alike. And then, over about ten days in November 2022, the whole edifice collapsed with stunning speed. It emerged that roughly $8 billion of FTX customers' money was simply gone — that the exchange had secretly funnelled its customers' deposits to Bankman-Fried's affiliated hedge fund, Alameda Research, which had gambled and lost much of it. There was no sophisticated technology failure and no clever scheme that merely went wrong; a court would find it was straightforward fraud and theft on an enormous scale. Bankman-Fried was arrested, tried, convicted on all counts, and in 2024 sentenced to 25 years in prison. This article tells the story of how a young man in shorts became the king of crypto, how he stole billions while presenting himself as the industry's most ethical figure, and how it all came apart in less than two weeks.