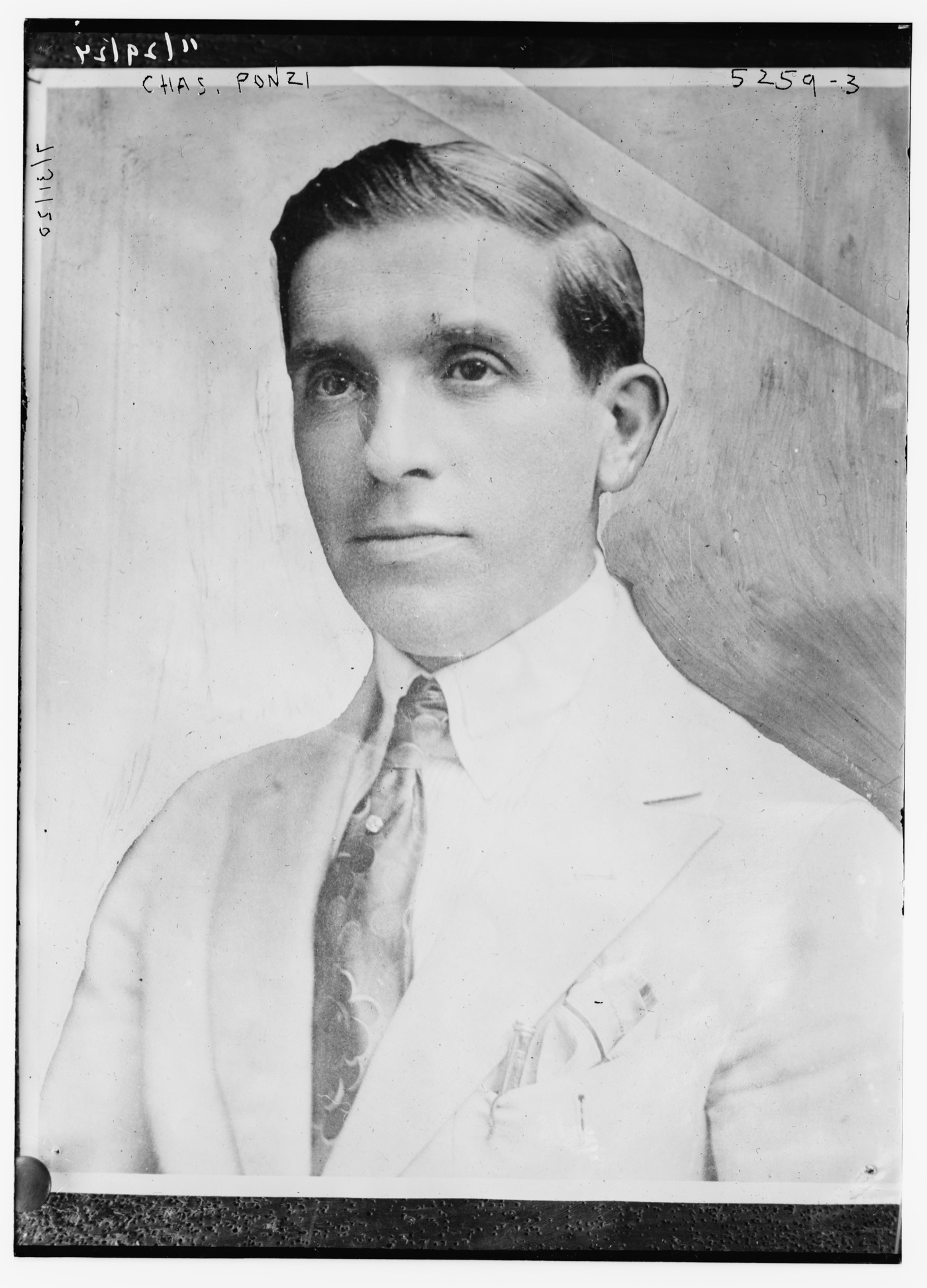

Charles Ponzi in 1920, at the height of his fame. For a few months he was the most celebrated man in Boston, promising to double his investors' money in ninety days. The scheme he ran — paying early investors with the money of later ones — was so spectacular that it took his name forever. Wikimedia Commons / Bain News Service, Public domain.

Charles Ponzi and the Scheme That Bears His Name

United States, 1919–1920 — An Italian immigrant in Boston promised to double your money in ninety days by trading postal coupons. There was no trading. There was only the oldest trick in finance, performed so spectacularly that it took his name forever

- Category

- Finance & Economy

- Published

- Length

- 4,105 words · 19 min read

- Author

- The editors

Almost everyone has heard the phrase "Ponzi scheme." Far fewer know that it belongs to a real man — a small, charming, relentless Italian immigrant who, for one extraordinary summer in 1920, convinced tens of thousands of ordinary people in Boston that he had found a way to double their money in three months. He had not. What he had found was something older and simpler: that if you promise spectacular returns and pay your first investors out of the money handed over by your later ones, you can manufacture the appearance of genius for as long as the new money keeps coming. Charles Ponzi did not invent this trick. But he performed it on such a scale, with such flair, and with such a spectacular collapse, that it has carried his name ever since.

This is the story of the man behind the scheme.

The man who would be rich

Charles Ponzi was born Carlo Pietro Giovanni Guglielmo Tebaldo Ponzi in Lugo, in northern Italy, in 1882. By his own later account he came from a once-comfortable family that had fallen on harder times, spent some money studying at university, and squandered the rest in the cafés and amusements of a young man with expensive tastes and little discipline. In 1903, at the age of twenty-one, he sailed for the United States, arriving — as he liked to tell it — with a few dollars in his pocket and a head full of ambition. "I landed in this country with $2.50 in cash and $1 million in hopes," he would say, "and those hopes never left me."

The years that followed were a long apprenticeship in hustle and disappointment. Ponzi drifted through a series of jobs along the eastern seaboard and into Canada — waiter, dishwasher, clerk, interpreter — and into trouble. In Montreal he worked for a bank that catered to Italian immigrants and collapsed amid fraud; soon afterward he was convicted of forging a cheque and spent time in a Canadian prison. Back in the United States he was imprisoned again for helping smuggle Italian immigrants across the border. By the time he settled in Boston in the later 1910s, married a young woman named Rose Gnecco, and tried to make an honest go of various small ventures, he was in his mid-thirties, ambitious, charming, and chronically broke.

What Ponzi had, in abundance, was a gift that no honest job had yet rewarded: he was likeable, quick, and persuasive, a small man with a big manner who could make the most improbable proposition sound not only plausible but inevitable. He needed only the right idea — something that could carry the weight of his ambition. In the summer of 1919, an ordinary piece of mail seemed to hand it to him.

The coupon and the dream

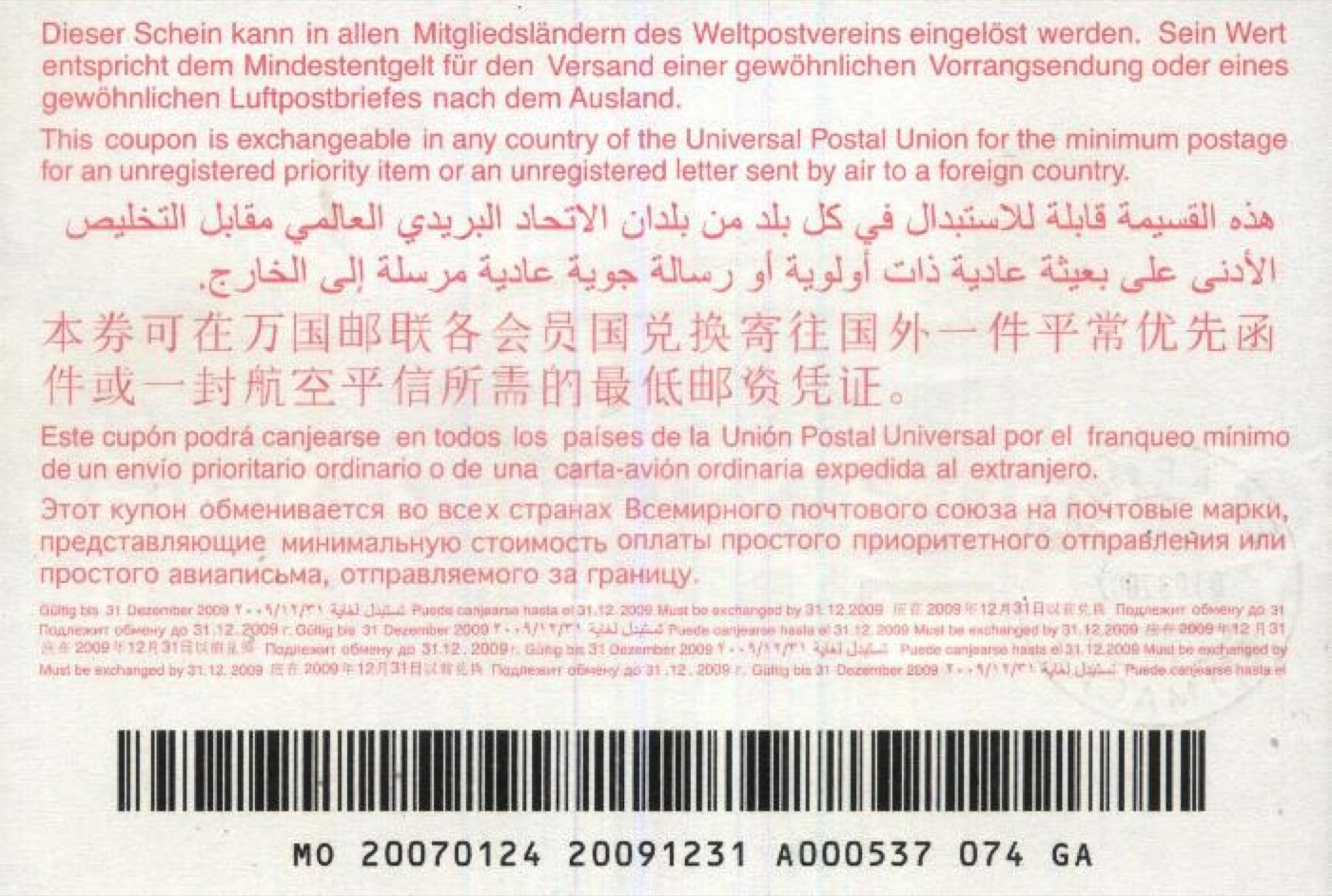

The idea arrived in the form of an international reply coupon. A correspondent abroad had enclosed one in a letter to Ponzi, who was at the time trying to launch a small business publication. An international reply coupon, or IRC, was a humble instrument of the global postal system: a person in one country could buy a coupon and enclose it in a letter, allowing the recipient in another country to exchange it for the postage stamps needed to reply, without having to pay for the return postage themselves. It was a small courtesy of international correspondence, designed so that a sender could prepay a reply across borders.

But Ponzi, examining the coupon, saw something else. The price of an IRC was fixed in the country where it was bought, and it could be redeemed for stamps at the local rate in the country where it was cashed. After the First World War, the currencies of much of Europe had collapsed in value against the US dollar. In theory, then, a coupon bought cheaply in a country with a devalued currency — Italy, say, or Spain — could be redeemed in the United States for stamps worth considerably more in dollar terms. Buy low in Europe, redeem high in America: a clean, legal arbitrage on the difference between fixed coupon prices and shifting exchange rates. Ponzi calculated that the gap could be enormous — that a coupon costing the equivalent of a penny abroad might be redeemed for many times that in American stamps.

The crucial thing about Ponzi's coupon scheme is that the arbitrage was not pure invention. The price gap was real; in principle, money could be made on it. This was what made the pitch so dangerous. A complete fantasy can be dismissed; a plausible half-truth, dressed in real figures and a genuine mechanism, is far harder to refute — and far easier to believe. Ponzi could point to actual coupons, actual exchange rates, actual postal regulations, and weave from them a story that sounded like the discovery of a money machine hidden in plain sight in the world's mailboxes.

What the story left out was that the arbitrage was, in practice, worthless at any meaningful scale. The coupons were of tiny denomination; to convert millions of dollars one would need to buy, ship, and redeem hundreds of millions of individual coupons. Postal authorities redeemed them only for stamps, not cash, and only in limited quantities; there was no legal way to turn a warehouse of stamps back into the fortune Ponzi was promising. The logistics were absurd, the transaction costs ruinous, the bureaucratic obstacles insurmountable. The money machine existed only on the back of an envelope. But by the time anyone worked that out, the machine Ponzi had really built — the one that ran on his investors' own money — was already roaring.

The Securities Exchange Company

In December 1919, Ponzi founded the Securities Exchange Company and began offering notes to investors. The terms were extraordinary: hand over your money, and in 45 days you would have it back with 50 percent interest; wait 90 days, and you would double it. He explained, when pressed, that the profits came from his coupon arbitrage, the details of which he kept deliberately vague — a matter of trade secrets, he implied, too valuable to disclose. To the first cautious investors, he made good on his promise: those who put in money got their spectacular returns, right on schedule, in cash.

That, of course, was the engine of the whole thing. The early investors were paid not from any coupon profits but from the money flowing in behind them, from the next wave of investors drawn by the first wave's astonishing good fortune. Each satisfied customer became a walking advertisement, telling friends and family and neighbours about the miraculous man on School Street who had doubled their money. The returns were real, in the sense that the cash was real; what was false was the story of where it came from. And because the scheme paid out so visibly and so reliably in its early months, the most persuasive evidence in Ponzi's favour was supplied by Ponzi's own victims, who could point to the dollars in their hands.

Through the first half of 1920 the operation grew from a curiosity into a phenomenon. Word spread through Boston's Italian community and then far beyond it, across class and neighbourhood lines. Police officers invested; so did clerks and labourers, widows and shopkeepers, the comfortable and the desperate. People remortgaged their homes, withdrew their savings, borrowed from relatives, all to get their money into Ponzi's hands before the opportunity closed. By the late spring the company was taking in staggering sums — by some accounts hundreds of thousands of dollars a day at the peak — and Ponzi had to hire clerks and open branch offices to handle the crush. Crowds filled the corridors outside his door, waving cash, and Ponzi, immaculate in his suits and straw hats, moved among them like a benevolent prince, reassuring, smiling, endlessly confident.

The rich man of School Street

For a few months, Charles Ponzi lived the life his million dollars in hopes had always promised him. He bought a fine house in the prosperous suburb of Lexington, complete with the trappings of wealth he had craved through years of poverty. He acquired a controlling interest in a Boston bank, the Hanover Trust Company — in part, it was later understood, to give himself a friendly home for his deposits and a veneer of financial respectability. He dressed beautifully, gave generously, and basked in a celebrity that the newspapers were happy to feed. Here was the immigrant success story in its most intoxicating form: the penniless arrival who had cracked the code of finance and was now showering his fellow citizens with riches.

Ponzi understood, with the instinct of a born performer, that the appearance of success was itself a kind of capital. The finer his house, the more spotless his suits, the more confidently he spoke of his coupon empire, the more credible the whole edifice became. He gave interviews, posed for photographs, and let it be known that he was contemplating grand philanthropies and vast new ventures — a bank of his own, a network of offices, an empire of finance built on the humble postal coupon. Boston, a city proud of its commercial history, found itself with a home-grown financial wizard, and for a heady stretch of weeks it chose to be dazzled rather than to ask the awkward question that hung over everything. Admiration, once it gathers momentum, does much of a swindler's work for him; the crowd's belief becomes self-reinforcing, each new investor reassured by the sight of all the others. Ponzi did not have to convince Boston one person at a time. He had only to keep the spectacle going, and let the spectacle convince itself.

But beneath the triumph the arithmetic was already closing in. Every note Ponzi sold was a promise to pay back far more than had been deposited, and every payout consumed the deposits of those who came after. A scheme of this kind is a race that cannot be won: to keep paying the older investors their 50 and 100 percent, the inflow of new money must keep accelerating, because the obligations compound while the underlying business produces nothing. For a while the acceleration held — the crowds grew, the deposits swelled — but the gap between what Ponzi owed and what he actually had was widening by the day. He was, even at the height of his wealth and fame, deeply and irretrievably insolvent. All that was needed to expose it was for someone to look.

The unravelling

Several someones did, more or less at once, in the summer of 1920. The first crack was a lawsuit: a furniture dealer named Joseph Daniels, who had once done business with Ponzi, sued him claiming a share of the profits, and in doing so drew public attention to just how much money Ponzi was supposedly making. The Boston Post, the city's leading newspaper, began to look more closely. Its acting publisher, Richard Grozier, and his editors smelled something wrong in the story of the miracle financier, and they began to investigate in earnest.

The decisive blow came from arithmetic. The Post consulted Clarence Barron, the respected financial journalist who gave his name to Barron's, and asked him to assess the coupon scheme. Barron's verdict was devastating in its simplicity. To back the tens of millions of dollars Ponzi had taken in, he pointed out, something like 160 million international reply coupons would have to be in circulation — when in fact only a tiny number, a small fraction of one percent of that, actually existed in the entire world. Moreover, Barron noted, Ponzi himself was not even investing his own money in the miraculous coupons; he kept it in ordinary bank accounts and conventional investments paying modest interest. If the coupon scheme were real, why wasn't its inventor pouring his fortune into it? The questions answered themselves.

As the Post pressed and the doubts spread, a run began. Investors who had been clamouring to put money in now clamoured to take it out, and lines formed outside the School Street office of people demanding their cash back. For a remarkable few days Ponzi met the run head-on, paying out millions to redeem notes, calm and smiling as ever, betting that visible solvency would restore confidence and stop the panic. To a degree it worked: some reassured investors put their money back in. But it could not work for long, because paying out the run only drained the reserves faster, and the underlying hole — the gap between what he owed everyone and what he actually had — was bottomless.

Then came betrayal from within. Ponzi had hired a publicity agent, William McMasters, to manage his image. But McMasters, examining the company's affairs from the inside, became convinced that his client was hopelessly insolvent and running a fraud. In early August 1920, McMasters took what he knew to the Boston Post, which published his account under his own byline: the man he had been hired to promote, he wrote, was "a financial idiot" who was massively in debt and whose scheme could not possibly be solvent. Coming from Ponzi's own publicity man, the exposé was catastrophic. The run resumed and did not stop.

The reckoning

The scenes outside the School Street office in those final days were the photographic negative of the mania that had preceded them. The same crowds that had pressed forward to hand Ponzi their cash now pressed forward to get it back, faces drawn with the dawning fear that they had been ruined. Many had invested not spare money but everything — the proceeds of a sold house, a lifetime's savings, money borrowed against the future. For these people the collapse was not an abstraction or a financial-pages curiosity but a personal catastrophe, and the human cost of the spectacle that had so entertained the newspapers was written in the anxious lines outside his door. It is a detail worth holding onto amid the period charm of straw hats and headlines: behind every Ponzi scheme, then and since, are real people whose trust is the raw material of the fraud and whose losses are its only genuine product.

State and federal authorities moved in. Massachusetts bank examiners and the United States district attorney's office began investigating, and an auditor named Edwin Pride was brought in to go through the company's books and establish the truth. His conclusion confirmed what Barron and McMasters had argued: Ponzi was massively insolvent, owing millions more than he possessed. The exact figures were tangled, but the shape was unmistakable — the Securities Exchange Company had no real assets generating profit, only a mountain of obligations to investors funded by an ever-shrinking pool of their own deposits. The Hanover Trust bank he controlled was seized by state regulators. In August 1920, Charles Ponzi was arrested.

The legal reckoning was long and tangled. Ponzi pleaded guilty to federal charges of using the mails to defraud and was sentenced to federal prison, serving several years. On his release he faced state charges in Massachusetts for larceny, was convicted after further legal wrangling and appeals, and went back behind bars. Even then his restless ingenuity did not desert him: while free on bail during the state proceedings, he turned up in Florida running a land-sales scheme, selling swampy lots to the gullible — another fraud, another conviction. He was, to the end, incapable of the honest, patient labour that his talents, honestly applied, might easily have rewarded.

By the time his sentences were served, Ponzi had spent years in prison and exhausted the patience of the country he had come to as a young man full of hope. He had never become a US citizen, and in 1934 the United States deported him to Italy. He left behind the wreckage of tens of thousands of ruined investors — though, in the final accounting, the trustees managed to recover and return to victims roughly thirty cents on the dollar, a partial mercy in a total disaster.

The long fall

The remainder of Ponzi's life was a slow descent. Back in Italy, he tried to attach himself to the Fascist regime and to various ventures, without lasting success. Eventually he made his way to Brazil, where for a time he found work connected to an Italian airline operating in South America. But the war disrupted those arrangements, and Ponzi, ageing and increasingly infirm, slid into poverty. His marriage to Rose had ended; his fame had curdled into notoriety; the million dollars in hopes had finally run out.

Charles Ponzi died in January 1949 in a charity ward of a hospital in Rio de Janeiro, partly paralysed and nearly blind, leaving barely enough money to cover his burial. He had, by one estimate, handled millions of dollars at the height of his scheme; he died with almost nothing. In a final interview not long before his death, he was unrepentant about the entertainment he believed he had provided. "Even if they never got anything for it," he reportedly said of his investors and the spectacle he had given them, "it was cheap at that price."

In the end, Charles Ponzi is less a villain than an archetype — the original of a type the world has met again and again. There was no real business behind his fortune, no secret discovered in the world's mailboxes, only the oldest illusion in finance performed with unusual flair: the promise of impossible returns, sustained by the money of those who believed it, for exactly as long as fresh believers kept arriving. He charmed a city, enriched himself briefly, ruined thousands, and died with nothing. But the lesson he left behind has outlived everyone who lost money to him, because it is endlessly relevant: when someone offers you returns that cannot be, and will not explain where the money truly comes from, the safest assumption is the one his investors learned too late — that the money comes from you, and from the next person through the door, and from no one and nowhere else at all.

Inspired this / based on it

Mitchell Zuckoff

Random House. The definitive narrative biography of Ponzi and his scheme.

Charles Ponzi

Ponzi's own self-serving autobiography, published from exile.

Filed under

- #charles-ponzi

- #ponzi-scheme

- #fraud

- #boston

- #postal-reply-coupons

- #securities-exchange-company

- #1920s

- #investment-fraud

- #boston-post

- #confirmed

Click any tag for every article carrying it.

Continue reading

Bernie Madoff and the Biggest Ponzi Scheme in History

Bernard L. Madoff was not a fringe hustler but a pillar of Wall Street. He had helped build the Nasdaq stock market and served as its chairman; he ran a respected market-making firm; he moved easily among the wealthy, the philanthropic, and the powerful. And alongside his legitimate business, he ran an investment-advisory operation that was, for decades, the envy of finance: a fund that delivered remarkably steady, positive returns year after year, in good markets and bad, never seeming to lose money. To be allowed to invest with Madoff was a mark of status, a privilege extended to wealthy individuals, charities, university endowments, banks, and feeder funds around the world. There was only one problem, and it was total: the investments did not exist. Madoff was not generating those steady returns by any strategy at all. He was running a Ponzi scheme — paying the 'returns' and redemptions of existing investors with the fresh money of new ones, while no real trading took place. For decades it worked, because as long as more money came in than went out, the scheme could continue and the statements could show whatever Madoff wanted them to show. When the financial crisis of 2008 triggered a wave of withdrawals he could not meet, the scheme collapsed, and the scale of it stunned the world: customer account statements showed about $65 billion that did not exist, built on perhaps $17–20 billion of real money that investors had actually handed over and that was now largely gone. It was the largest Ponzi scheme in history. And the most damning detail of all was that a financial analyst named Harry Markopolos had been telling the Securities and Exchange Commission, repeatedly and in detail, for nine years, that Madoff was a fraud — and had been ignored. This article tells the story of the respectable man who ran the biggest financial fraud ever, the warnings the watchdogs missed, and the lives it destroyed.

Enron and the Most Innovative Company That Never Really Made Money

For six consecutive years, Fortune magazine named Enron the most innovative company in America. The Houston-based energy company had, the story went, transformed itself from a sleepy operator of natural-gas pipelines into a dazzling new kind of business — a trading powerhouse that bought and sold energy and almost anything else, light on physical assets and heavy on financial genius, the very model of the modern corporation. Its stock soared; its executives were celebrated as visionaries; its revenues, on paper, rocketed past $100 billion. And then, in the autumn of 2001, it all came apart with breathtaking speed. It emerged that Enron's reported profits were substantially an illusion, manufactured through aggressive and deceptive accounting; that the company had hidden enormous debts and losses in a web of hundreds of secretive off-the-books entities, some named after Star Wars characters; and that the 'innovation' the world had admired was, to a damaging degree, the art of making a company that did not really make money look as though it made a great deal. In about six weeks, Enron went from a $60 billion blue-chip giant to the largest corporate bankruptcy in American history to that point. Twenty thousand employees lost their jobs and, in many cases, their retirement savings, which had been tied up in Enron stock. Its auditor, Arthur Andersen — one of the five great global accounting firms — was destroyed in the fallout. The scandal sent executives to prison, prompted landmark reforms, and became the defining symbol of corporate fraud at the turn of the millennium. This article tells the story of how the most admired company in America turned out to be a confidence trick, and how the trick unravelled.

Nick Leeson and the Rogue Trader Who Broke a 233-Year-Old Bank

Barings Bank was an institution almost synonymous with British financial respectability. Founded in 1762, it had financed the Napoleonic Wars and the Louisiana Purchase, served the British monarchy, and survived for 233 years as one of the City of London's most venerable merchant banks. In February 1995, it ceased to exist — destroyed not by war or recession but by a single trader on the other side of the world. Nick Leeson, a 28-year-old from a working-class background, ran Barings' futures-trading operation in Singapore, and he appeared to be a star, generating spectacular profits that made him one of the bank's most valued employees. In reality, he was concealing catastrophic losses in a secret error account numbered 88888, doubling down again and again on losing bets that the Japanese stock market would stay stable. The bank's management, dazzled by his apparent success and failing utterly to supervise him, kept sending him money to cover his positions, believing it was funding profitable trades. Then, on 17 January 1995, a massive earthquake struck the Japanese city of Kobe, sending the Tokyo market into turmoil and turning Leeson's enormous bets disastrously wrong. As the losses ballooned past the bank's entire capital — ultimately around £827 million — Leeson fled, leaving a note that read 'I'm sorry.' Within days, Barings was bankrupt, sold to a Dutch bank for one pound. This article tells the story of how one unsupervised young man, a hidden account, and an earthquake brought down a bank that had stood for nearly two and a half centuries — and what it revealed about the dangers of trading without control.